How Much Does a Title Search Cost? State Fees Explained

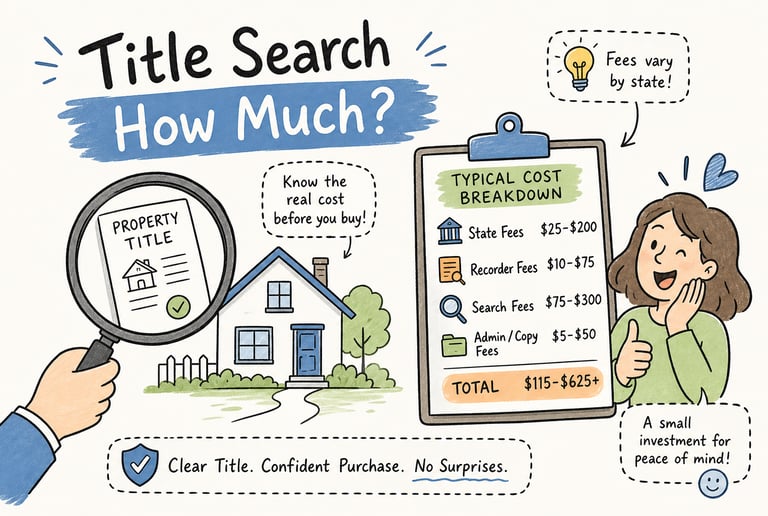

Title search costs vary widely by state, county recording practices, property type, and search depth; residential searches commonly run $75–$250 (most $100–$200), complex homes $300–$600+, commercial searches $1,000–$2,500+, and O&E (Owners and Encumbrances) searches $55–$175. Blazer Title Search breaks down state-by-state ranges and what’s included so you can judge whether a quote is reasonable.

REAL ESTATE TITLE SEARCH

Nick Thomas

6/5/20266 min read

How much does a title search cost? Call three title companies for a quote and you'll likely get three different numbers. That's not a coincidence or a sales tactic. Title search pricing is genuinely variable, and the reasons for it are specific and knowable. At Blazer Title Search, the single most common question we get is some version of "how much should this cost me?" The answer depends on a handful of real factors, once you understand them, you can estimate your own cost with confidence.

This article gives you actual numbers broken down by state, property type, and search depth. You'll know what's included in the fee, what gets billed separately, who typically pays it, and what moves the price up or down. By the end, you won't need to wait on a callback to know whether a quote is reasonable.

What a Title Search Actually Costs on Average

For a standard single-family home, the national baseline for a residential title search runs from $75 to $250 (as of 2026). Most straightforward deals land somewhere between $100 and $200. "Straightforward" means a recent purchase, clean ownership history, no probate or trust complications, and a county with accessible digital records. When those conditions exist, the search is efficient and the price reflects that.

Commercial properties and complex residential cases operate on a different scale entirely. Commercial title searches routinely start at $1,000 and climb to $2,500 or higher depending on parcel count, ownership entity complexity, and transaction scope. For residential deals, older properties with long chains of title, inherited homes, or properties with a foreclosure history can push costs to $300 to $600 or more. The baseline is real, but complexity is always priced in.

New York commands a premium because urban title records in the metro area are layered and historically complex. Florida trends toward the lower end of residential fees but climbs quickly with distressed or tax deed properties. Illinois fees spike in Cook County the same way New York fees spike in the five boroughs: dense urban markets with older records cost more to search. Title report cost can vary by county even within the same state, sometimes dramatically. For additional context on national cost trends and examples, see Orchard's analysis of title search costs.

How County Recording Practices Drive the Price

This is the mechanism most buyers don't understand. Some counties maintain well-indexed, fully digitized records going back decades. Others require an abstractor to physically pull documents at the courthouse. That hands-on time is labor, and labor is cost. Rural counties, older urban counties, and states with no statewide recording standardization tend to be the priciest markets for search work. Two properties in the same state can carry very different search fees simply because one sits in a county with modern online access and the other doesn't.

How Much Does a Title Search Cost by State?

Geography is the biggest pricing variable most people don't account for. Title company fees vary significantly depending on where the property sits. Here's how fee ranges break down across major states for the title search itself (not including title insurance, recording fees, or other closing costs):

The Factors That Push Your Quote Higher (or Keep It Low)

How Much Does a Title Search Cost: O&E vs. Full Search

The type of search you order is the single biggest pricing lever. An O&E (Owners and Encumbrances) search covers only the current owner's period of ownership. It's the right tool for tax deed investors, pre-foreclosure due diligence, and many investor acquisition checks. It's faster, less labor-intensive, and meaningfully cheaper, typically $55 to $175 depending on the county. A full title search going back 30 to 60 years is required when title insurance will be issued on a purchase transaction. It takes more time and costs more because more records are examined.

Conflating the two is where investors consistently overpay. Ordering a full 30-year search on a deal that only warrants an O&E is a real and avoidable cost leak. Matching the search type to the actual transaction is the first cost control decision you make. For a practical primer on why O&E reports and full searches serve different purposes, review FastTitleSearch's guide to O&E reports versus full title searches.

Property History and Chain-of-Title Complexity

A home that transferred cleanly three times in the last decade is a fundamentally different search than a property that passed through an estate, sat in a trust, had a tax lien, and changed hands in a foreclosure. Each stop along the chain of title is a link the abstractor needs to verify. More links, more time. More time, higher fee. A property with a foreclosure and estate transfer in its history might run $350 to $500 where a clean transfer runs $150, and this is what drives most of the variation buyers don't expect.

What's Actually Included in That Fee vs. What's Charged Separately

The title search line item pays for the labor of locating, pulling, and examining public records tied to the property. That includes deeds, mortgages, liens, easements, judgments, and tax records. Some providers include supporting documents alongside the report; others charge extra for copies. At a minimum, the search should produce a clear chain of title and a documented list of any encumbrances found. At Blazer Title Search, supporting documents are included with every report as standard, not an upsell.

Title insurance is a separate product entirely. It protects against losses from title defects that the search missed or that surface after closing. It's priced separately, always. Recording fees, settlement or escrow fees, attorney fees in attorney-state closings, and notary fees are all separate line items as well. One of the most common confusion points for buyers is seeing "title fees" as a bundled total on the Loan Estimate and assuming the search is included, only to find it itemized separately on the Closing Disclosure. They're distinct charges for distinct services. For a clear breakdown of how lenders and closing statements typically handle title-related charges, see Rocket Mortgage's guide to title fees.

Who Pays the Title Search Fee and How It Shows Up at Closing

In most states, the buyer pays for the title search as part of closing costs. In states like Illinois and Wisconsin, the seller customarily pays. Florida generally has the seller paying, though this varies by county and deal structure. Local convention matters more than any national rule here, and in many transactions, especially off-market investor deals, this line item is openly negotiable and gets worked into the offer terms directly.

The search fee appears in Section C of the Closing Disclosure under "Services You Can Shop For." That language is important: it signals that you're legally permitted to choose your own title search provider rather than using whoever the lender defaults to. Most buyers don't realize this. Choosing an independent provider is one of the clearest ways to reduce this fee, and you have the legal right to do it. For practical buyer-facing guidance on essential title fee considerations before closing, consult AmeriSave's essential facts about title fees.

How Investors Running Multiple Deals Manage Title Search Costs Efficiently

The cost control approach for investors starts with ordering the right search type for each deal. A tax deed purchase, a pre-foreclosure letter campaign, or an initial acquisition check doesn't require the depth of a full purchase closing search. Identifying which product fits which transaction, before you order, reduces spend without reducing the information you actually need.

The second problem is friction in getting quotes. Different counties have different requirements, different turnaround windows, and different pricing. Calling around to gather quotes across multiple jurisdictions is genuinely time-consuming, and it makes it hard to build a predictable cost model across a deal pipeline.

Blazer Title Search built a state- and county-specific pricing tool to eliminate that friction. You select your state and county and get an instant flat-rate estimate without a single phone call. For investors placing multiple orders per month across different jurisdictions, that kind of pricing transparency changes how you underwrite and how you plan.

Volume investors also benefit from knowing that not every deal needs the same service level. A preliminary investor check, a full pre-foreclosure search, and a purchase closing search are each a different product at a different price point. Knowing which one you need, and ordering accordingly, is how experienced investors keep title search costs proportional to the deal rather than defaulting to the most expensive option every time.

What to Take Away from All of This

The national range is $75 to $250 for a standard residential title search, with commercial and complex cases going significantly higher. State and county are the biggest variables, with New York and California markets at the upper end and Florida trending lower for straightforward deals. The type of search matters as much as location. An O&E search and a full 30-to-60-year search serve different purposes and carry different price tags.

So how much does a title search cost for your specific deal? Know what's included in the title search fee, know what's billed separately, and know that Section C of the Closing Disclosure gives you the right to shop for your own provider. For anyone doing multiple deals per month, pricing transparency isn't a convenience, it's a planning tool. Blazer Title Search's county-level pricing tool gives you that number instantly, so you can work it into your underwriting before you make an offer rather than after you're already under contract. The number is there before you need it. That's the point.