Liens on a Title Search: Full Breakdown for Buyers

Learn which liens appear on a title search, how recorded and unrecorded claims differ, and what to check to avoid costly surprises at closing.

REAL ESTATE TITLE SEARCH

Nick Thomas

6/29/20268 min read

Pulling a title report is one of the first real tests of whether a deal is worth pursuing. It tells you what you're actually buying, the full encumbrance history, not just what the seller says you're buying. Understanding what types of liens show up on a title search before you make an offer is the difference between a clean close and a legal headache that costs you time, money, and sometimes the deal entirely. Many properties carry at least one lien, and some carry several, layered over years of ownership, court judgments, unpaid taxes, and contractor disputes. The ones you don't find in advance are the ones that hurt you at closing.

What liens appear on a title search depends on three things: the property's history, the owners connected to it, and the type of search you ordered. A basic current owner search finds different things than a 30-year full title search. Services like Blazer Title Search are built for this specifically: surfacing a property's full encumbrance history before you're committed to anything.

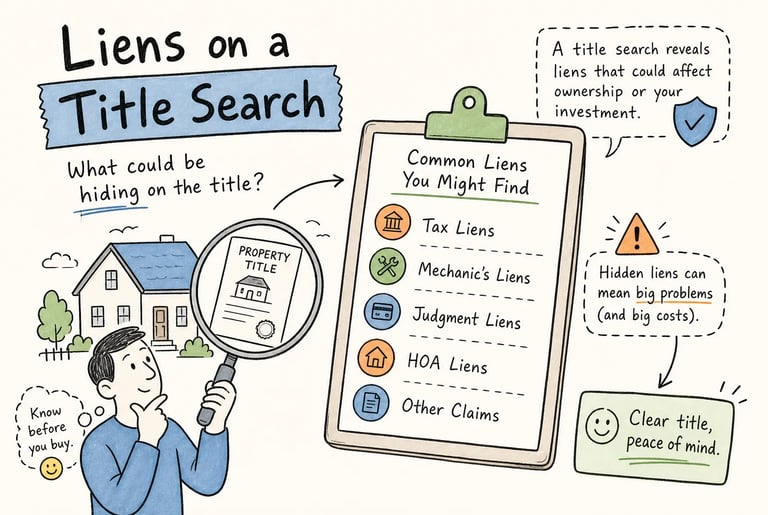

What Types of Liens Show Up on a Title Search: Recorded vs. Unrecorded

The most important distinction in any title search is this one: recorded liens live in county public records and are legally visible to any buyer. Unrecorded liens don't appear in those records and are generally not enforceable against a bona fide purchaser without notice, but certain municipal charges can still create enforceable obligations under state or local law and may be collectible by the municipality even after a sale. If you don't know the difference, you can close on a property thinking it's clean and find a five-figure municipal debt waiting on the other side. For guidance on how to find recorded and unrecorded liens on a house, consult a detailed title-search resource before you bid or sign.

What gets captured in a county title search

A standard county title search pulls from recorder and clerk of court databases to surface all formally filed encumbrances: mortgages, tax liens, judgment liens, mechanic's liens, and HOA liens. A thorough search maps these to the property's ownership chain and includes the supporting documents behind each filing. The title search report gives you more than a list of lien names. You're looking at the actual recorded certificates, judgment filings, and tax notices that tell you exactly what you're dealing with and who holds each claim.

The hidden category: unrecorded municipal claims

A standard title search won't catch utility bill arrears, open building permits, code violations, or nuisance abatement charges. These are real liabilities. Fines for unresolved code violations can accrue daily and in some cases reach thousands of dollars or more. Worse, certain municipal charges may follow the property after the sale under local law. For investors buying distressed properties or anything in a dense urban market, a separate municipal lien search isn't optional. It's a basic part of due diligence that most people skip until they get burned once.

Mortgage liens and voluntary encumbrances

Not every lien is a red flag. Mortgage liens are voluntary, meaning the property owner agreed to them as a condition of financing. They show up on virtually every title report for a property that was ever financed. The key question for an investor is simple: can the outstanding balance be satisfied from the sale proceeds, and has every prior mortgage been properly released?

How mortgage liens work and when they clear

When a borrower takes out a loan, the lender records the mortgage in county public records. When the property sells, the title company orders a payoff demand, the balance is settled at the closing table, and the lender files a reconveyance or release. For investors buying cash or at auction, the verification step matters: confirm that prior mortgages were actually released, not just assumed to be gone because the loan was old.

What to watch for in the lien history

Title reports sometimes surface old mortgages where the release was never formally recorded, even though the loan was paid off years ago. These appear as open liens until someone files the release with the county. A solid title search flags these so the seller can obtain the documentation needed to clear the cloud before closing. This is a common issue on properties that changed hands multiple times or went through informal transfers.

What Types of Liens Show Up on a Title Search: Tax Liens

Tax liens are where investors need to pay the most attention. There are two distinct categories, local property tax liens and federal IRS tax liens, and they work differently. Local property tax liens carry true super-priority status in virtually every state, ranking ahead of nearly every other creditor, including first mortgage holders. Federal IRS liens are powerful and far-reaching, but they generally rank below state and local tax claims. Both categories appear on a comprehensive title search, and both can stop a deal if they're not addressed before closing.

Property tax liens: local government's first claim

When a property owner fails to pay real estate taxes, the county records a tax lien. Because these carry super-priority status, they outrank even an existing first mortgage. Leave them unpaid long enough and the county can proceed to a tax deed sale. Investors looking at distressed properties need to identify outstanding tax balances early in their review, since these amounts must be resolved before the title can transfer cleanly.

Federal IRS tax liens: the 10-year clock

IRS liens arise from unpaid federal income taxes and, once filed, attach to all property the taxpayer owns, not just the subject property. A Notice of Federal Tax Lien is recorded in the county where the taxpayer holds real estate and remains valid for 10 years from the date of assessment, with possible extensions. If a property sells, the IRS has a 120-day window after the deed transfers to exercise certain rights under applicable statute. Run a federal lien check on every deal, regardless of how financially stable the seller appears. Ownership history is rarely as clean as it looks on the surface.

Judgment liens, mechanic's liens, and HOA claims

These three involuntary lien types are the ones that most often blindside investors, especially on properties with a complicated history or recent renovation work. They're all recorded in county records, which means a solid title search will surface them. Understanding how each one works separately is what lets you evaluate the risk quickly and price it into your offer.

Judgment liens: when a court ruling follows the property

A judgment lien is created when a creditor wins a lawsuit and records the judgment in the county where the debtor owns property. It attaches to all real property the debtor holds in that county. These liens can surface years after the original lawsuit, and if the property changed hands informally or the owner relocated, the chain gets complicated fast. Duration varies by state, typically five to twenty years, though some states set shorter windows, and the lien must be formally satisfied or released before the title can transfer free and clear.

Mechanic's liens: contractor claims and their tight windows

When a contractor, subcontractor, or supplier performs work on a property and doesn't get paid, they can record a mechanic's lien against the title. These are particularly relevant for investors buying properties that saw contractor activity in the past year or more. Mechanic's liens have strict filing deadlines, as short as 90 days in California and up to one year in Florida, and expire if the claimant doesn't pursue foreclosure within the statutory window. Even so, an expired mechanic's lien that was never formally released still clouds the title until someone files the release with the county.

HOA liens: small balances with real consequences

HOA liens arise from unpaid dues, fines, or special assessments in homeowners' associations. They may seem minor compared to a tax lien, but they attach to the property and must be cleared before closing. In some states, HOA liens carry a limited super-priority status that places them ahead of a first mortgage for a portion of the unpaid balance. Investors buying properties in planned communities, condominiums, or gated neighborhoods should verify HOA standing as part of every title review, not as an afterthought.

Lien priority: the payoff order that determines your real exposure

Priority determines who gets paid first when a property sells or goes through foreclosure. This is where the difference between a manageable deal and a losing one often lives. The equity you think is in a property can disappear quickly once you map out the order in which claims get satisfied.

The general priority hierarchy and its exceptions

The baseline rule is first in time, first in right: the lien recorded earliest takes priority over later ones. But statutory exceptions override this in important ways. Local property tax liens hold super-priority in virtually every state, meaning they're paid first regardless of when other liens were recorded. Federal IRS liens generally rank above private mortgage liens but below state and local tax claims. Mechanic's liens in many states relate back to the date work began, which can push them ahead of mortgages recorded after construction started.

Why priority matters before you make an offer

Consider a property with a first mortgage, a federal tax lien, and a judgment lien. Which gets paid first from the sale proceeds determines whether there's any equity left for the investor after the debt stack is satisfied. When liens exceed the property value, that's a deal-stopper unless the investor can negotiate payoffs or buy at a steep enough discount to account for the senior claims. Priority is both a legal concept and a financial calculation; it belongs in every offer analysis. For a primer on What is a Title Search and Why Every Deal Needs One, consult a focused explainer before you run numbers.

Clearing liens before closing: who pays and how it works

Once a title search identifies the liens on a property, the work shifts to resolution. Most liens are paid from seller proceeds at the closing table, but the documentation requirements and timelines vary by type. Knowing what each resolution looks like helps investors set realistic closing timelines and avoid last-minute surprises that kill otherwise clean deals.

The resolution process for each major lien type

Mortgage liens are satisfied through a payoff demand and a recorded reconveyance from the lender. Tax liens require a clearance certificate from the taxing authority before the title transfers. Judgment liens need a formal satisfaction of judgment filed with the county clerk after payment or negotiated settlement. Mechanic's liens are resolved through payment, settlement, or bonding around the claim. HOA liens are cleared with a payoff statement from the association. In every case, the lien release must be filed with the county recorder to remove it from the title record, even after the underlying debt is paid in full.

How Blazer Title Search helps investors get ahead of these issues

For investors who want this level of detail without building an in-house research process, a purpose-built title search service is the practical answer. Before you make an offer, an Owner and Encumbrance (O&E) search or a Full Title Search through Blazer Title Search can surface recorded liens, judgments, unpaid taxes, and ownership discrepancies along with the supporting documentation behind each finding. For pre-foreclosure situations, a 2-Owner Report can help identify prior claims that may complicate noticing or deed applications. Knowing what liens show up on a title search before the negotiation starts, not after, is what keeps you from pricing a deal wrong or closing into someone else's liability. For deeper reads, check the Real Estate Title Search: A Complete Guide for Investors and our practical How to Do a Title Search on a Property (Complete Guide).