O & E Title Search: What It Covers and When You Need It

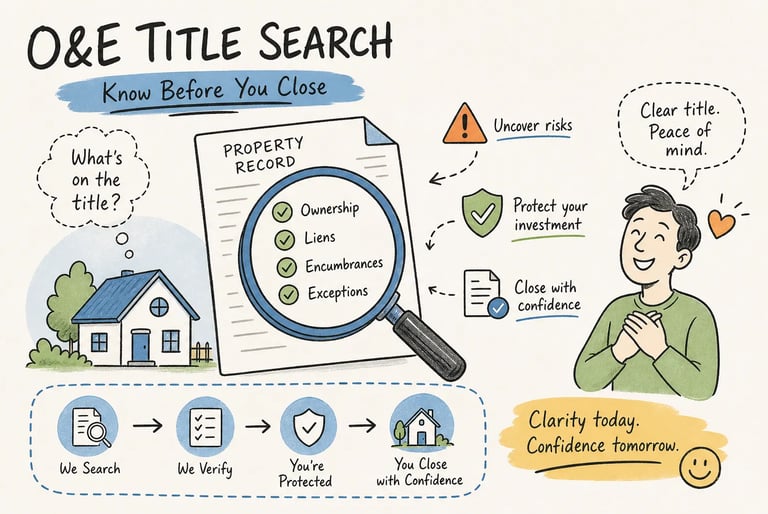

An O&E (Ownership and Encumbrance) report gives a fast, affordable snapshot of who currently owns a property and what recorded claims or restrictions attach to it, highlighting unreleased mortgages, tax liens, and judgments. It's an informational due-diligence tool—not title insurance—so investors and attorneys can decide whether to proceed or require a deeper search.

REAL ESTATE TITLE SEARCH

Nick Thomas

6/20/20269 min read

You've found a deal. The price looks right, the numbers work, and you're ready to move. But you have no idea what's actually attached to that property. There could be an unreleased mortgage from a decade ago, a federal tax lien, or a judgment sitting on title that would land in your lap the moment you close. That's the exact problem an O&E title search is built to solve.

An O&E, or Ownership and Encumbrance report, gives you a fast, clear picture of two things: who legally owns the property right now, and what recorded claims or restrictions are tied to it. It's a practical due diligence tool used by real estate investors, attorneys, and title professionals to understand the current state of a title before committing to a deal. It's not a title insurance policy, and it doesn't certify that title is clean. What it does is put the facts in front of you so you can make an informed decision.

This article covers everything you need to know about O&E reports: what they include, how they're performed, what they cost, and when to order one instead of a full search.

What an O&E title search actually is

An Ownership and Encumbrance report is a Current Owner title search. An O&E is a limited, informational title search that captures the current owner of record and all active encumbrances tied to a property. Think of it as a snapshot: it shows where things stand right now, not the entire 30-to-60-year ownership chain going back to prior transactions. That narrow scope is what makes it fast and affordable, and it's also what makes it the right tool for specific situations rather than every situation.

An Ownership and Encumbrance report is not a title insurance commitment. It doesn't certify marketable title, and no underwriter is standing behind it. It's a research output based on the public record as of the search date. That distinction matters, especially for investors who sometimes assume a clean O&E report means they're fully protected.

The two core components: ownership and encumbrances

Ownership covers who holds title now, how title vested to the current owner (sole ownership, joint tenancy, an LLC, a trust), and the legal description of the property. The vesting deed is included so you can see exactly how title transferred to the current party. Encumbrances are every recorded claim or restriction attached to that property that a buyer would inherit or need to resolve before or at closing. The report lists recorded matters found in the public records searched that fall within the scope of the O&E, though inclusion can vary by provider and search parameters.

Why it's informational, not insurance

An Ownership and Encumbrance report is a research tool, nothing more. It tells you what the county record shows as of the search date. Title insurance requires a deeper search, a formal examination, and a commitment from an underwriter who is pricing the risk of insuring that title. An O&E gives you the facts and leaves the judgment call to you. For many investor transactions, that's exactly the level of information needed to decide whether to proceed or walk away.

What shows up on a typical O&E report

When the report lands in your inbox, here's what you're actually looking at: the vesting deed, the legal description, and a rundown of all open encumbrances found in the public record. The supporting documents that back up each finding should come with the report so you're not just reading a summary without context. For examples and explanations of common formats, see owner's encumbrance reports that illustrate typical outputs and supporting documents. Owner's encumbrance reports

Open mortgages and unreleased deeds of trust

Any mortgage not formally released in the county record still appears as an active encumbrance, even if the underlying loan was paid off years ago. Unreleased mortgages are one of the most common surprises investors find on O&E reports. The prior lender may have been paid in full at closing, but if no release or satisfaction was ever recorded, the lien technically still exists on the title. That's a defect that needs a cure before or at closing.

Tax liens, judgments, and HOA assessments

Federal tax liens filed by the IRS, state tax warrants, and court-ordered money judgments against the owner all attach to real property and can survive a sale if they're not addressed. HOA and condo association assessment liens work the same way. All of these appear on an O&E report, and all of them become your problem if you acquire the property without resolving them first. For tax deed investors especially, surfacing these items before the auction is the entire point of ordering the report.

Easements and deed restrictions

Recorded easements, utility, access, or drainage rights held by neighboring property owners or utility companies, don't block a sale but they do affect how you can use the property. Deed restrictions and covenants that run with the land, including HOA rules and use limitations, are also recorded encumbrances. These items matter for investors evaluating development potential, renovation scope, or long-term hold strategy.

How an O&E search is performed, and who does it

The process is more systematic than most investors realize. A title abstractor or examiner pulls the relevant county records, confirms the parcel through tax data and GIS, traces the recorded deeds to confirm current ownership, and then searches for all liens and encumbrances in the county recorder's index. The findings get compiled into a report, and supporting documents are pulled alongside it.

From property identification to compiled report

The search starts with confirming the correct parcel using the property address, parcel ID, and tax records. From there, the examiner reviews recorded deeds to confirm how title vested in the current owner. The lien search then pulls mortgages, judgments, tax liens, HOA assessments, and any other recorded claims from the county index. Everything gets organized into a clear report, with the actual recorded documents included so findings can be verified.

Who performs the actual search

Title abstractors and examiners do the hands-on record review. Title companies and title search providers like What is a Title Search and Why Every Deal Needs One | Blazer Title Search coordinate the process and deliver the finished report. Attorneys step in when a legal defect needs resolution or when the transaction itself requires legal oversight, such as in a quiet title action or contested foreclosure. Investors and attorneys typically order directly from a title search provider rather than going through a full-service title company for this type of report.

O&E vs. full title search: picking the right one

This is the decision most investors get wrong, either by over-ordering and paying for depth they don't need, or by under-ordering and relying on a limited snapshot when the transaction demands a full chain of title. The right call depends entirely on what you're doing with the property.

Most title search providers offer tiered report options designed for different use cases: a current-owner or O&E search, a two-owner or pre-foreclosure report, and a full title search covering 30 to 60 years. Each product is built for a specific scenario. Blazer Title Search structures its offerings the same way, so you're only paying for the depth your transaction actually requires. Unlike a standard ALTA title search, which involves a comprehensive chain of title and is typically required for lender transactions, an O&E report is scoped to current ownership and active encumbrances only.

When an O&E report is the right call

Tax deed auctions are the clearest use case. You need to know who owns the property and what's on title before you bid, and you need that information fast. The same logic applies to tax lien investing, wholesale and assignment deals, pre-foreclosure noticing, and quick property screening before making an offer. In these scenarios, speed and current-status accuracy matter more than a 60-year ownership history. An O&E title search gives you exactly what you need without the cost or timeline of a deeper search. For guidance on applying title searches to higher-risk investments and auctions, see Navigating High-Risk Property Investments with Title Searches | Blazer Title Search.

When you need a full title search instead

Traditional purchase closings, lender-required title insurance, and quiet title actions all require a 30-to-60-year chain of title. If a title company needs to issue a formal insurance commitment, they need the full history, not a current-owner snapshot. Cutting corners here creates real liability: older defects, missing heirs, and recording errors from prior transactions won't show up on an O&E report, but they can still cloud title after you close.

What an O&E search costs and where to order one

Budgeting is straightforward once you understand the range. Most standard O&E reports for real estate investors fall between $90 and $135, with the broader market ranging from roughly $55 to $275 depending on the state, county, and complexity of the search. Rural counties with older or less digitized records can push costs higher, while straightforward residential parcels in active counties tend to land at the lower end of that range.

Typical cost ranges to expect

Pricing transparency varies by provider. Some title search companies, including Blazer Title Search, offer county-specific pricing through an online selection tool so you know the exact cost before you place an order. For investors running due diligence on multiple properties across different counties and states, that kind of upfront visibility is genuinely useful. It also makes it easier to build title search costs into your underwriting from the start.

Turnaround times and when rush service matters

Turnaround varies widely across providers and markets. Many O&E reports come back within one to two business days, while more complex files or counties with older records can take up to a week or longer. Blazer Title Search typically delivers most reports within two to four business days, with rush service available for time-sensitive auctions or closings (see Rush title search: when real estate investors need one | Blazer Title Search). For practical timing expectations across different counties, see this overview of how long a title search takes. How long does a title search take? Many providers include supporting documents alongside the report summary as standard, though practices vary, so it's worth confirming with your provider before you order. When you're evaluating a deal on a tight timeline, having the actual recorded documents in hand alongside the report summary makes a real difference.

What to do when the O&E report finds problems

Finding open liens or defects on a report isn't a reason to panic. Most of these issues are solvable, and the cure paths are well established. The report surfacing a problem is a good outcome, it means you found it before you closed, not after.

Common defects and how they get resolved

For paid-off debts where the lender never recorded a release, the fix is obtaining and recording a mortgage satisfaction or lien release from the original lienholder. Recording errors in prior deeds get corrected through a corrective deed or affidavit. Ownership disputes involving missing heirs or informal transfers typically require a quitclaim deed, an affidavit of heirship, or probate proceedings depending on the facts. More complex competing claims, where multiple parties assert ownership rights, usually require a quiet title action filed in court. The title company or attorney directing the closing typically manages the cure process and confirms the defect is cleared before closing proceeds.

When title insurance becomes necessary

If a buyer is financing the purchase, the lender will require a title insurance policy regardless of what the O&E report shows. That requirement applies to every financed transaction without exception. Owner's title insurance is optional but strongly recommended when the title history is murky, when defects were recently resolved, or when the property came through a tax deed or foreclosure process where older claims could re-emerge. The O&E report is the starting point: it tells you what's there. Title insurance is the protection layer that follows, covering you against claims that couldn't be found or weren't recorded as of the search date.

Know before you bid, buy, or close

An O&E title search is the fastest, most cost-effective way to verify current ownership and surface active encumbrances before you commit to a deal. It's not a substitute for a full search in every situation, but for real estate investors, tax deed buyers, pre-foreclosure work, and property screening, it's usually exactly what the transaction calls for.

The investors who get burned on title issues aren't always the ones who skipped due diligence entirely. Often, they're the ones who assumed the deal was clean without actually checking. An O&E report is how you check. It typically takes a few business days, costs under $100 in many markets, and tells you what you need to know before you're on the hook.

If you need a reliable O&E report with fast turnaround and county-specific pricing, Blazer Title Search is built for exactly that. Use the online pricing tool to get your county's rate and place your order at BlazerTitleSearch.com.